Week 39: Timing is Everything

Early or late = wrong

Hi. Welcome back to Fifty Trades in Fifty Weeks

This is Week 39

50in50 uses the case study method to go through one real-time trade in detail, about once per week. This Substack is targeted at traders with 0 to 5 years of experience, but I hope that pros will find it valuable too. For a full description of what this is (and who I am), see here.

If you want to learn about global macro in real-time … subscribe to my daily: am/FX

Listen to this as a podcast on the web … or Spotify … or Apple.

Update on previous trades

Week 38: Medium-term short vol trade in MSTR is fine, no real update.

Week 37: XOM put spread doing OK.

Week 36: TGT dumped and WMT didn’t dump enough. L.

Week 35: Short MSTR in the money, not moving much. Left an order to square it up at $160.55 last week. Almost there!

Week 34: EWZ call spread is bad.

Full update with the detailed spreadsheet next week (Week 40.)

Don’t forget to buy yourself a holiday gift by subscribing to am/FX.

Timing is Everything

There is a cliché in trading: Early is the same as wrong. Most people understand this, but there should also be a saying: Late is the same as wrong. Putting on trades too early or too late has both real and opportunity costs.

This week, I am going to expand on the lessons from Week 38 and show you another way to use options to help with the structuring and tactics of a trade idea.

It’s (no longer) raining yen

The big trade of 2023 was supposed to be long JPY. In early December, I did a survey of am/FX readers and here is the currency they most wanted to be long:

The main driver of the bullish JPY thesis was an expected pivot from the Bank of Japan (BOJ).

BOJ Governor Kuroda leaves at the end of March 2023 and his Yield Curve Control (YCC) program has been the catalyst for an epic moonshot in USDJPY this year. By pinning Japanese yields super low (around 0.25%) while US yields have exploded higher to around 4.0%, Kuroda engineered a massive rip higher in USDJPY (115 to 150 this year). Investors generally prefer currencies with higher yields, most of the time.

If you are an investor, and you are trying to maximize returns, you are generally happier holding a bond that yields 4% vs. one that yields 0.25% (all other things being equal).

The presumption is that if the BOJ loosens the cap on yields and allows Japanese yields to go higher, Japan’s yields can rise to catch up with the rest of the world and that will make the JPY more attractive (or at least… Less unattractive).

Here’s USDJPY since I sent out the survey:

USDJPY 15-minute chart since early December

137 to 131 in one day is a large move!

The BOJ changed its YCC program ahead of schedule, raising the top of the yield control band from 0.25% to 0.50%. USDJPY got slammed! Many hedge fund managers and spot traders out there were busy wargaming all the USDJPY puts they planned to buy in January, and now the move they expected in Q1 2023 has already started.

It’s like everyone was off to the side tying their shoes and stretching their calves when the starting gun went off.

This led to a lot of FOMO trading as people walked in and saw USDJPY at 131.25 and decided they had better get on board. The problem was, the daily chart looked like this:

USDJPY daily chart back to mid-2021

At the time, I tweeted:

Traders and portfolio managers were selling hard, right into major support. They were late for the first move and compounded the problem through reactionary selling. Now they are early for the next leg. Here is the updated chart:

USDJPY hourly chart back to late November

Trading is all about timing. When you’re early, you get chopped up by the noise and bleed theta. When you are late, you miss the juicy part of the move and get sucked into good trades at bad levels. Tactics are an absolutely critical part of trading and you have to resist the urge to sell into collapsing markets or buy explosions out of FOMO.

It’s not always wrong to go with the momentum, but if you’re going to chase momentum you need to do it in a thoughtful, strategic way. Always ask yourself whether your trading strategy is about tactics and rational thinking, or FOMO and price chasing.

Another reason the rush to buy USDJPY puts after the BOJ announcement is risky: USDJPY puts got significantly more expensive because of the surge in demand. The way you look at the price of puts vs. calls in FX is the price of the risk reversal.

The simple interpretation of the risk reversal is that it tells you the price of USDJPY calls relative to the price of USDJPY puts. When demand is high for one side of the market, that side will get more expensive. This is also called skew. The more demand there is for options in a particular direction, the more difficult that direction is to hedge, and the less natural selling there is of those options, the more expensive options in that direction will be.

S&P puts, for example, are almost always more expensive than calls because there are tons of natural buyers of puts (portfolio hedgers, specs, etc.) but few natural sellers. Selling S&P puts is very difficult to risk manage and there are only limited participants who can do so.

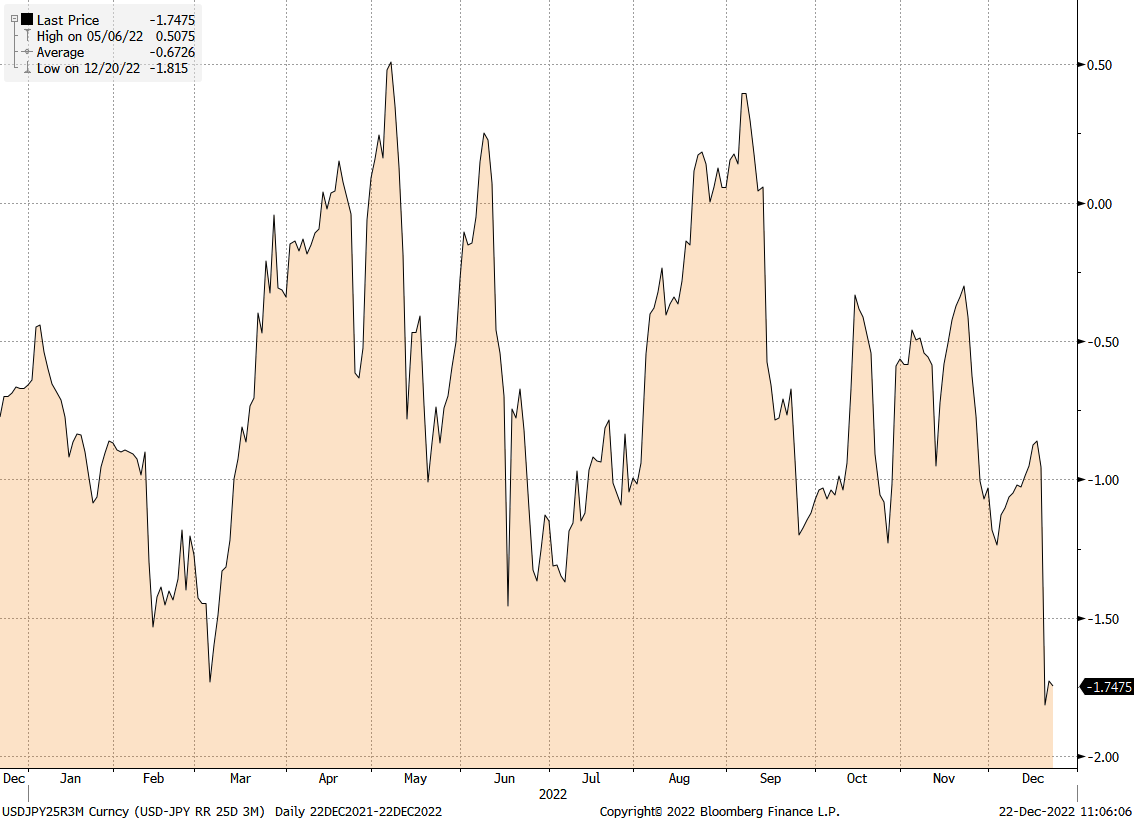

Here is the USDJPY risk reversal. You can see how the line moved down dramatically in the last few days. When that line goes down, it means that USDJPY puts are getting more expensive.

USDJPY 3-month 25-delta risk reversal since late 2021

So not only did spot USDJPY drop 500 points, but your puts are going to cost much more today than they did a few days ago.

A timing trade

Now that the Bank of Japan has signaled a willingness to move its 10-year yield target, one might expect the JPY to appreciate in 2023. That is, the consensus narrative for JPY strength in ‘23 has been somewhat validated by Kuroda’s actions. On the other hand, you can also argue that a nearby catalyst (change in YCC) has now passed and the market has already repriced from 137 to 132 in one day.

What is the best way to play it going forward? You missed the first move, so do you want to chase it? Or do something else?

My view is that now that the YCC move has happened, we will consolidate, and USDJPY will range trade for a while. Then, once the market finds out who the new BOJ governor is in February, it will be game on again and USDJPY will skate lower.

When you have a directional view, and a strong sense that the timing of the directional move will happen not now, but later, it’s a good setup for calendar spreads.

Calendar spreads are a simple options strategy where you sell an option for one date and buy an option for another date. In order to avoid outright short volatility exposure, for me this always means selling a nearer-dated option and buying one farther out. That way, if things move dramatically, you are protected. You are net long options.

For example, you sell a USDJPY put for expiry in February 2023, and buy one that expires in June 2023. This cheapens up the strategy significantly compared to simply buying a June 2023 option and allows you to benefit from the consolidation, instead of paying time decay.

I am going to go through the details here using over-the-counter FX options, but the concepts are identical whether you use options on CME futures or even options on a yen-tracking ETF like YCS. All the concepts apply to retail or institutional trading of any options product.

The strategy

Let’s say we think USDJPY will be at 120.00 at the end of June 2023. A 6-month 125 USDJPY put costs about 2.00%. You can sell a 2-month 125 USDJPY put for around 0.65%.

So if you do these two options (buy 6-month and sell 2-month) you pay about 1.35% instead of 2.00% (that is: 2% minus 0.65%). The dream scenario is that USDJPY is exactly 125.00 in two months so the option you’re short expires worthless and the one you are long is at the money.

Calendar spreads are a good strategy to keep in mind for any market you trade. As I said last week:

Owning outright volatility (vol) all the time is wrong-way risk for your trading P&L. Directional short-term traders make more money when things are moving and volatility is high. So you are already exposed to volatility by this reality. If vol is high, your trading will be more profitable, on average. Active traders are implicitly long vol. So if you always buy vol via options, you are adding to the risk of a boring market that makes trading harder, and bleeds you out on time decay.

Buying options requires an exciting market. If you buy calls and then the market takes a nap, you’re losing money even if you’re directionally right.

Calendar spreads are still “owning volatility” but you are doing it in a more nuanced way.

If you are bearish TSLA but think it’s oversold right now and set to consolidate… Either wait for better levels or do a calendar spread. If you think MSFT is going to do nothing into earnings, then beat and explode higher; do a calendar spread. The risk with calendar spreads is that you can be right and lose money but there’s always a variety of risks around every execution style and trading outright long vol comes with its own huge bag of risks, too.

You have to accept that sometimes you will be correct and still lose money. That’s just part of trading.

The current head of the BOJ, Kuroda, was nominated on February 27, 2013. His term expires at the end of March 2023 and therefore the Japanese government will need to nominate a new governor at some point in February. If Nakaso is nominated, that would be hawkish (higher yields) and therefore good for the yen (bearish USDJPY). Other candidates could have varying impacts on the direction of BOJ policy and USDJPY. Here is a quick story that will give you the background on possible choices:

https://www.japantimes.co.jp/news/2022/12/12/business/boj-leadership-candidates/

One note about risk and execution. If USDJPY goes below 125 before the 2-month option expires, I will be exercised and end up with a potentially large USDJPY position. Usually if I am near my short strike as expiry gets close, I will roll or unwind the option to avoid exercise. Whenever you trade option spreads, make sure you understand the exercise risk and what happens to your margin if you get exercised.

And one final technical note and another reason selling 2-month to buy 6-month is nice: Due to the carry in USDJPY, the strike on the 2-month ATM USDJPY put is about 200 points higher than the strike of the ATM in the 6-month.

Conclusion

Timing is everything in trading. While in bubbles and massively trending markets, timing can be temporarily less important, it is generally critical to trading success. Many young traders made their first foray into trading in the 2020 bull market. And in parts of 2020 and 2021, timing was almost irrelevant. Everything was going up all of the time. You could buy calls on just about any stock, wait a couple of weeks, and hit the take profit button.

2022, was a mirror of 2021, somewhat, but timing became more important. Despite strong trends like USDJPY higher, stocks lower, EURUSD lower, etc., timing was key. If you were selling the hole in stocks or EURUSD in 2022, you were bearish and you got smoked despite a trending bear market. As global macro (including stocks and everything else) enters a more uncertain regime in 2023, timing and direction will both be paramount to success.

Strategies like calendar spreads increase the complexity of tactics and pose new risks not posed by other strategies, they can also be the best way to express a view. If you think USDJPY is going to hang around 128/132 for a while and then trend lower starting in February, it makes sense to sell a 2-month 125 USDJPY put and buy a 6-month 125 USDJPY put.

The most important takeaway, though, is to make sure you are trading rationally, and not out of FOMO or frustration. If you can step outside yourself and see yourself trading on FOMO, you will be able to course correct and stop the behavior or correct it before it costs you too much capital.

This concludes Week 39. Thank you for reading.

If you liked this week’s 50in50, please click the like button. Thanks.

Trade at your own risk. Be smart. Have fun. Call your mom.

And don’t forget to buy your 2023 Trader Handbook and Almanac.

DISCLAIMER: Nothing in “50 Trades in 50 Weeks” is investment advice. Do your own research and consult your personal financial advisor. I’m putting out free thoughts for people who want to learn. This is an educational Substack. Trade your own view!

If you are passionate about learning how to trade…

Sign up for my global macro daily, am/FX, right here

Subscribe to 50in50 for free right here.