Hi.

Welcome to Fifty Trades in Fifty Weeks! This is Trade 2: Short oil.

Click the play button above to read this idea with your ears.

Thank you for signing up!

50in50 uses the case study method to go through one real-time trade in detail, about once per week. This Substack is targeted at traders with 0 to 5 years of experience, but I hope that pros will find it valuable too. For a full description of what this is (and who I am), see here.

I am a huge believer in the case study method. It gives you the tools to find answers instead of the answers themselves. It teaches people how to fish instead of handing them a plate of sashimi.

If you would like to read more about the case study method (which is celebrating its 100-year anniversary), check out this article from HBR.

Trader Error

Oops.

Last week, 50in50 went short XAUEUR (short gold vs. euro) and I didn’t put “Russia invades Ukraine” on my list of risks. That is a fail on my part. It was a known risk, but unfortunately, it had been kicking around for a few weeks and I failed to take it into account. That’s not good.

A few people asked if I would exit the trade or hedge it, etc. but this being a weekly blog, I will not be dynamically hedging or rebalancing. While I want to approach realism here, I only have so much time and the incremental value add of monitoring and updating in real-time is not worth the massive increase in effort.

The purpose of this letter is not to create a real-time portfolio of winners.

The purpose of this letter is to explain the process of trading. Whether I am writing a Substack or managing a $400 million hedge fund portfolio, I always try to focus on process, not outcomes. That is the winning approach in trading, poker, golf, and any probabilistic pursuit. A golfer can practice, prepare, center her mind, go through all her mental exercises, step up to the tee… And still shank the ball into the pond. That’s just how life goes. Focus on process and not on outcomes.

By the way, process over outcome is a great way to live a less stressful life and it’s also the thesis of the book “Thinking in Bets” by Annie Duke. I highly recommend that book to anyone serious about trading or poker.

Before we get to the trade idea, a fairly detailed explainer is in order as I outline how I use correlation to trade. I introduced a few correlation concepts last week when I explained how negative-yielding debt and US real rates are correlated to the price of gold. Today, I am going deeper into cross-market correlation, continuing with some themes from Trade 1.

I watch all markets and attempt to make sense of what micro moves in markets might mean for forward-looking global macro.

Correlation is useful, even when it’s not causal

Whenever I point out a less obvious correlation between two markets, the most common skeptical reaction is “correlation does not imply causation”. Tyler Vigen’s famous website has some excellent examples of strong correlations between series that are clearly not causal. These are called spurious correlations. Here’s one:

The word spurious means “not being what it purports to be; false or fake.” But is this correlation spurious?

Well, there is certainly no causation between ice cream sales and shark attacks. People do not get attacked by sharks because sharks smell ice cream in swimmers’ bellies, right? But the relationship is not a nonsensical coincidence, either.

There is a third variable (seasonality) that drives both series. During the summer, people go swimming more, get attacked by sharks more, and buy more ice cream. Outdoor temperatures drive both series and generate the high correlation.

Another correlation like this would be “Starbucks Pumpkin Spice Latte advertising budget vs. Buzz Lightyear costume sales.” Both spike around Halloween. Seasonality can also drive markets. For example, natural gas prices rise in winter as demand peaks.

Stock markets also exhibit persistent seasonality and (much to the dismay of the haters and the EMH acolytes), that seasonality works in and out of sample, across almost every geography, for the past 300 years. The next chart shows the average seasonality of US stocks since 1990 in light blue along with the actual path that stocks took in 2021 (dark blue). Amazing!

This is not hindsight… I was writing about this in am/FX in September 2021 as a reason to be bearish and in mid-October as a reason to be bullish. Like every input, seasonality is not the be-all, end-all… It’s one of many clues. It works on average, but not every year of course.

S&P 500 Average Seasonal Performance and 2021 Performance

There are many third variables that can drive financial markets. For example, Canadian interest rates, Canadian equity markets, and the Canadian dollar will all move in predictable ways in reaction to Canadian GDP growth and inflation. If growth in Canada is strong and there is high inflation, you would expect Canadian yields, equities, and CAD to do well. This is a simplistic view of the world and not always true, but it’s a good starting point.

Most markets move up and down in response to the same underlying drivers, such as:

Economic growth and inflation

Monetary Policy

Geopolitics

Global risk appetite

So there is a reason that markets are correlated. People yelling “CORRELATION IS NOT CAUSATION!” in all caps are technically right but practically not very helpful. There often is no causation, but there is a ton of information contained in the correlation between assets.

Here are six other ways the abstract concept of cross-market correlation plays out in the real world.

1. Arbitrage and substitution. This is an easy one in its simplest form. If bitcoin is selling at 57,500 on one platform and there is a bid at 57,600 on another platform, that’s pure arbitrage[1]. There is also a more nuanced version of this that looks a lot like arbitrage but is not. This is usually called basis or RV trading.

Closest to arbitrage is the basis between two fungible or nearly-fungible products like futures and spot. You can sell gold futures and buy physical gold and at some point down the road, the prices are very likely to converge. This is not arbitrage though! There is a significant basis and mark to market risk. Still, this basis-related near-arbitrage is the reason nearly-fungible products like futures and spot, or ADRs and their underlying stock price, exhibit very high correlation.

Moving along the spectrum from arbitrage to basis to RV… If you build a curve of all the crude oil futures prices and there is a kink in the curve that puts the DEC 2023 high relative to the other contracts, you can sell DEC and buy a contract on or below the curve and have an excellent (but not risk-free) chance of making money.

Substitution is further out on the same spectrum. This is the dynamic where a rise in the price of one asset will lead consumers to buy a cheaper substitute. If corn doubles in price, those who can switch to soy will do so, pushing the price of soy futures higher. If Doordash rips higher and now looks overvalued, investors looking for food delivery apps to invest in might buy GrubHub instead.

2. Third variable. As briefly mentioned above, when two asset prices move up and down together, they could be responding to a third variable that drives them both. This is the most common driver of the correlations I talk about and it is the reason trading lead/lag is logical. Most of the assets moving around on your screen are responding to the same set of macro stimuli.

As outlined above, if there is rising optimism about Canadian growth, CAD will trade stronger, and Canadian interest rates will rise. The third variable (Canadian growth expectations) is the key driver of both USDCAD and Canadian rates. This will show up as high correlation between the two markets and the snazzy overlays that frequently decorate am/FX.

Opportunities arise as some markets move more slowly than others and the signal from one market provides clues as to the direction of the other. This could be because of non-price-sensitive flows against the grain in one market but not the other.

For example, if the outlook for China growth is improving and copper is ripping higher but a huge M&A is going through selling AUD, you might see a divergence develop. The moment the M&A transaction is complete, AUDUSD will snap higher to where it “should have been” given the rally in copper and the rosy outlook for China.

3. Cash flows. When one asset moves, it can generate cash flows in another asset. For example: When a Canadian crude oil producer sells their crude, they receive USD. They need CAD to pay their employees and shareholders so after they sell their crude, they need to sell USDCAD to convert the proceeds. If the price of crude doubles, the crude producer will have twice as many USD to sell and this will weigh on USDCAD.

This is one mechanism that drives the USDCAD vs. crude oil correlation. If you have ever worked at a bank with a strong Canadian presence, you know those flows are an important piece of the USDCAD puzzle.

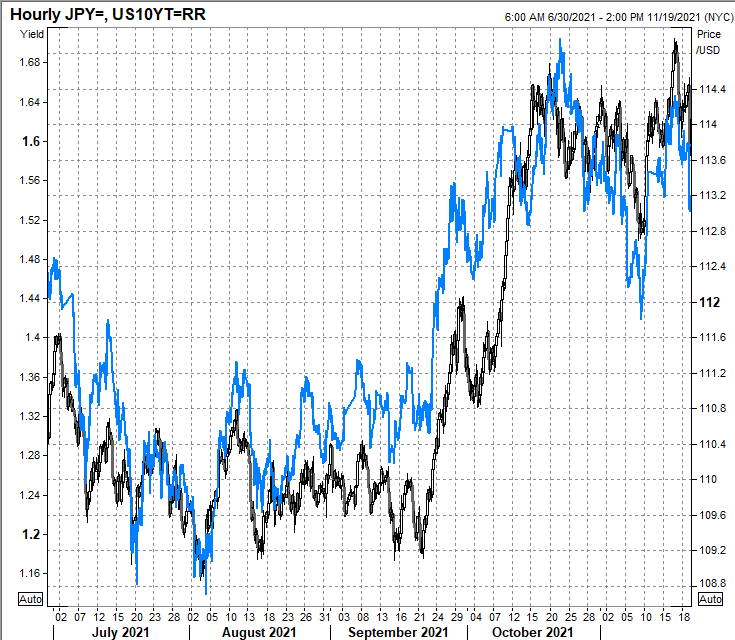

While cash flows are a significant driver of the correlation between commodity currencies and commodities, cash flows can also be important in other pairs. If US yields move higher, Japanese investors will find those higher yields appealing and will buy US bonds. Those purchases will drive the USD higher and generate a correlation between US yields and USDJPY.

Higher yields tend to, but do not always, lead to higher USDJPY.

USDJPY vs. US 10-year yield, July to November 2021

4. Cross ownership / liquidation / forced selling. Speculators tend to take positions relating to broad macroeconomic themes. For example, at the moment the theme is inflation so the macro positions are: short bonds, long USDJPY, long oil, and so on. When there is significant movement in one of those assets (even if views on the global growth outlook have not changed), it will trigger activity in the other markets as owners of the basket react to the changes in their P&L.

For example, if the market is positioned short bonds and long oil for the inflation trade (like they are right now), and bonds start to rally. You might see oil start to sell off as speculators feel the pain in their P&L. The more bonds rally, the more oil specs need to sell to manage their drawdown.

5. Correlation traders and algos (self-fulfilling prophecy). Since people know that certain products are correlated, they won’t wait for the cash flows or cross-ownership flows to kick in. If oil rips $2 higher, algos and humans all over the world will sell USDCAD.

6. Volatility and systemic risk. As systemic risk rises and risky assets fall, correlations rise. Every asset has an idiosyncratic risk component and a systemic or macro risk component. Idiosyncratic risk (say, supply and demand for copper) loses importance when systemic risk is high. Intense risk aversion pushes all correlation towards one as the only thing that matters is the rise or fall of the systemic risk.

Like many high school relationships, correlations are fun, but unstable, and unreliable. They can bring you great joy and inspiration one day and then leave you sad and confused the next. That is why I never present correlation factors as the be-all-end-all. They are the clues that might get you to a good idea, but they are never the answer.

Trading is probabilistic, not deterministic.

No matter how confident you are in your trade idea, always know there’s a pretty good chance you might still be wrong. This gives you incredible freedom because once you acknowledge and accept you are going to be wrong rather frequently, you get used to it. It becomes part of the process and you don’t really take an emotional hit when you stop out. There are no sure bets in trading and if you are 100% confident on a trade, or it seems like free money, you are probably about to get punched in the face by Mike Tyson.

That’s the intro. Now let’s get to the idea. I will keep it pretty tight from here because I promised you each 50in50 would be under 3000 words.

First, a quick word from our sponsor.

Today’s 50in50 is sponsored by Brent Donnelly’s daily global macro newsletter, am/FX. Get Brent’s views on global macro (including live trade ideas) in your inbox, every single day. You will also get occasional creative brilliance, dumb facts, huge Excel grids, and video game/book recommendations.

Subscribe to am/FX here

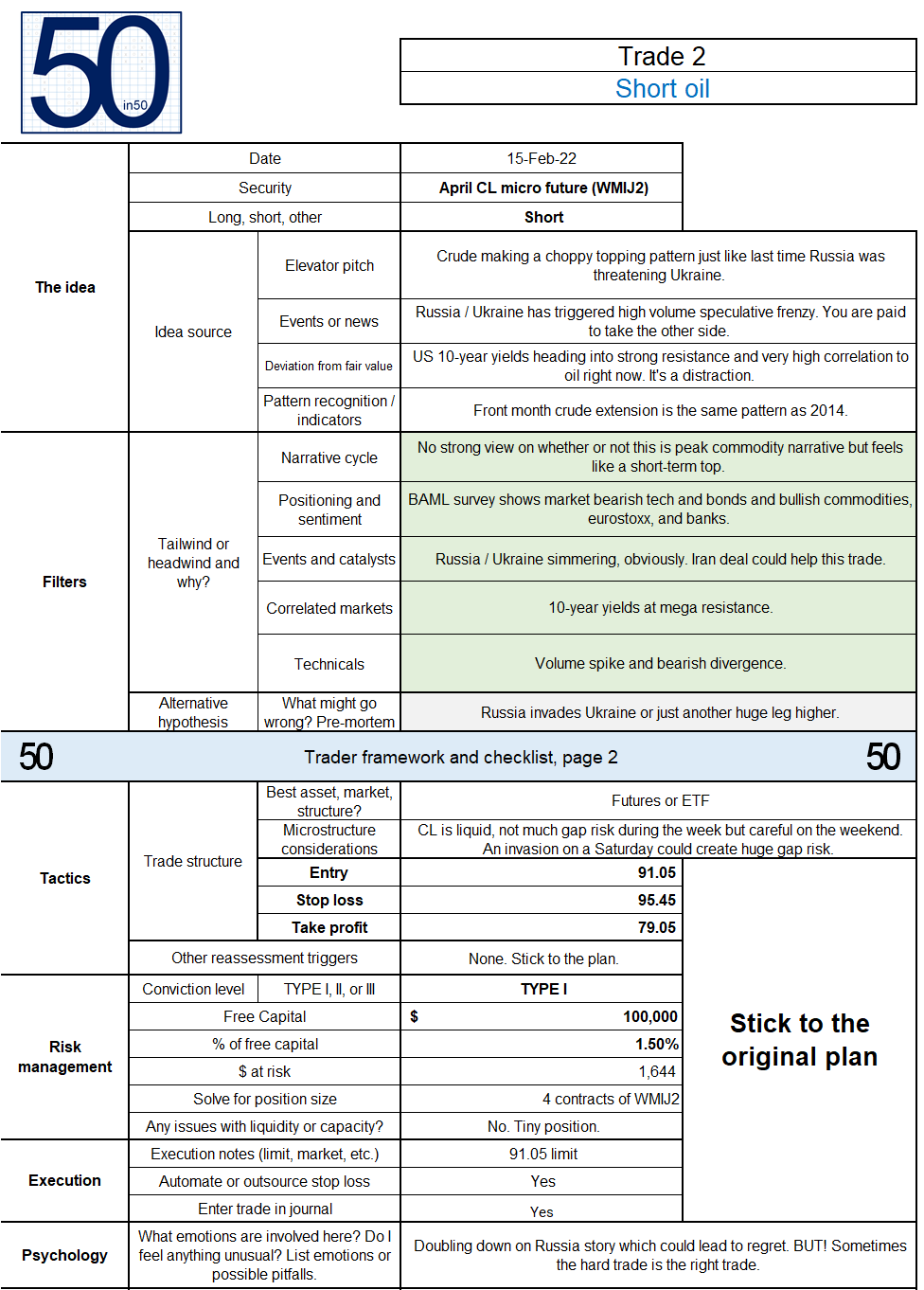

Trade 2: Sell oil

Here’s my completed framework template for this sell oil trade.

Get your own blank one here as PDF or here as XLS.

I am using micro oil futures in the spreadsheet because the position size is too small for regular futures. CME micro futures are 1/10th the size of normal ones. Note, I am not an expert in retail execution (!!) so make sure you know what you are doing before you trade. None of this is investment advice. This is an educational product. Seriously.

Figure out how much you want to risk in $ and then back out your position size as explained in 50in50 #1. Here is a futures P&L calculator. There is a chance I could make a mistake when discussing particular products like micro crude futures, which I am familiar with conceptually, but have never traded because I worked at a bank or hedge fund for most of my life.

Here’s a quick run through of the logic of the trade. Note, this is not a big picture global macro trade. It’s a quick attempt to pick a top in a market that looks like it’s blown off to the topside. Risking 4 dollars to make 12.

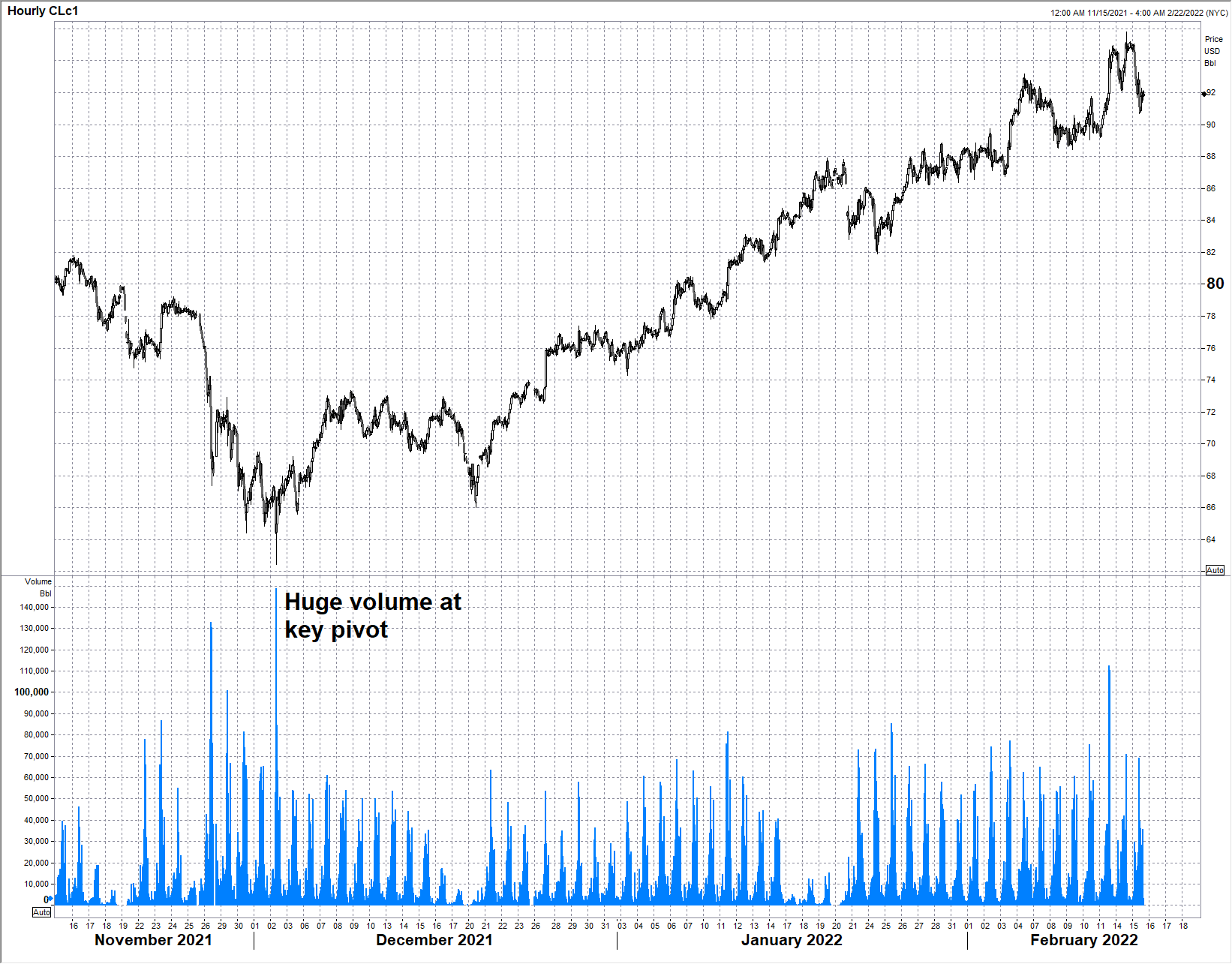

Blow-off top on high volume

As you can see from the chart, the hourly volume in crude futures this week hit a three-month spike high. Spikes in volume can often be indicative of panic and forced buying or selling and they make great turning points. When there is a massive surge of volume and the price rejects that location, you can then pinpoint that location as a critical pivot. In this case, it’s the high. Then, you set your stop loss above that. Note the sweet, sweet megavolume low in early December.

Crude oil fails on huge volume spike

Front end contracts megabid but contracts further out not so much

There are dozens of crude oil futures contracts that expire as early as this month and as late as 2033. You can plot a curve of the prices and sometimes it slopes up and sometimes it slopes down. Here’s the curve right now.

A deep dive into the importance of the shape of the crude curve is beyond the scope of this piece, but believe me when I say a steep downward slope like that is rare. The next chart gives you a sense of some history.

This chart shows the first contract (CL1) minus the contract that expires five years later (currently 93 minus 68 = 25 approx). When crude markets are tight and there are shortages, you tend to see the first contract trade at a huge premium. Generally, that is unsustainable and it’s a sign of unsustainable upward price pressure.

Front NYMEX crude (CL) minus CL contract expiring in five years

Pull up a chart of crude oil and you will see that prior times when the front end was super bid (late 2013, 2014, and 2018) were horrendous times to own crude. Extreme moves in the crude curve tend to (but do not always) signal potential mean reversion.

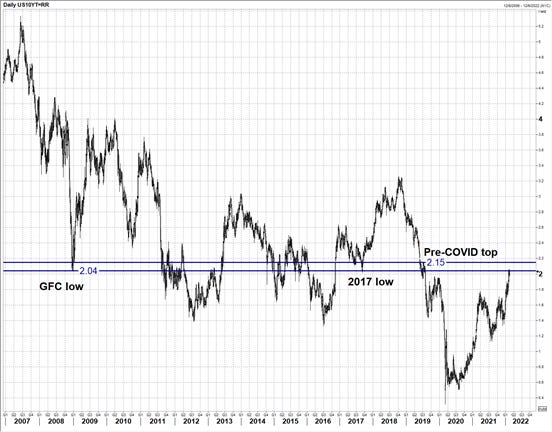

US 10-year yields entering massive resistance zone

US 10-year yields and crude oil have been moving in lockstep for months.

And we are entering a big zone of interest here in US 10-year yields. 2.04% was the post-GFC low and the 2017 low (see chart) and the last spike higher before the Fed started easing then COVID hit was 2.15%. As such, I think 10-year yields will start to struggle up here. The implication, given the correlation between rates and oil, is that if yields slow their ascent, the entire reflation trade will too, and that should take a bit of pressure off oil.

US 10-year yields in a big resistance zone

And, finally, the Economist is asking “How High Will Interest Rates Go?” which can often, but not always, be a contrarian indicator.

I would never trade off any single one of the reasons I have listed here today, but in combination, this looks like a nice setup. If you are wondering why the Economist cover is contrarian, full explanation is here.

Risks

This is another Russia invasion risk trade, in theory. I don’t really believe that a Russian invasion means much for crude beyond a kneejerk reaction, but the market seems to think so. The good thing about this setup is that Russia invasion odds have shot higher and you are now selling AFTER the high volume spike and failure in crude. If oil can get back up and make new highs, it deserves to stop me out!

There is a positive kicker risk on this trade: If there is a deal on Iran nuclear, that could bring more supply to market and hit oil.

I put this as a TYPE I trade because it is correlated risk to Trade 1 and because my conviction is a bit lower given the risk of a random headline that could take me out at the knees without warning. Then again, I like placing trades like this where you have a very clearly-defined exit level and a good entry point.

It’s way too complicated for me to consider the 50in50 trades as a portfolio, so generally, I will NOT be factoring in the correlation between live 50in50 trades. It’s way too complicated and boring for this Substack.

I don’t know retail trading platforms

The point of this Substack is not to teach you the micro specifics of how to press buttons on your specific platform. I want to explain to you the general idea and you figure out how to do it on Interactive Brokers or TD Ameritrade or whatever platform. I’m no expert on that. I worked as a market maker at a bank and traded OTC for most of my life and even when I traded futures in the past, it was at a hedge fund.

Be very careful with your weekend risk. A stop loss doesn’t help you much if you’re short at $91, Russia invades on Saturday and you get filled at $101. Either square up on the weekends, or size it so you are not ruined by a $15 or $20 weekend worst-case scenario gap. Unlikely but pointless risk.

If you want to do this trade, micro CL futures should work, but you could also structure it your own way through Brent crude, XLE, or whatever else is correlated to crude oil. I used April micro futures (WMIJ2 on Bloomberg) because March futures are about roll off. That’s why my entry point is $91.00. There will sometimes be small lags by the time I send out the piece so don’t freak out if my entry is slightly different from the market when you get the piece :]

Trade idea summary:

TYPE I conviction sell oil futures

Short-term blowoff top on high volume gives a nice entry

The curve is steep like it was at prior highs

Correlated asset (yields) entering massive resistance

Final thoughts

Some will not like this trade because I am doubling down on Russia risk. I think it’s worth it.

I have to say of the 100s of geopolitical flare-ups I have seen (including the March 2014 annexation of Crimea)… Very few have had a lasting impact on markets.

I acknowledge that this is like saying “very few earthquakes destroy cities.” When it happens, it’s a massive deal but you can’t spend the rest of 2022 under the desk hiding from Putin. He might stack the border with materiel for the next 12 months in a Sword of Damocles kind of strategy. If Russia invades, my trades will get stopped out. That’s life.

Thank you for reading!

brent

If you need moar Brent Donnelly in your diet, check this out this podcast or better yet, sign up for my daily!

Subscribe to am/FX here

[1] Here is an excellent trading story involving arbitrage. Probably my favorite trading story of all time.

{kind=link}